Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

These 8 beginner-friendly emergency fund plans make saving money feel realistic, manageable, and way less overwhelming even if you are starting from zero.

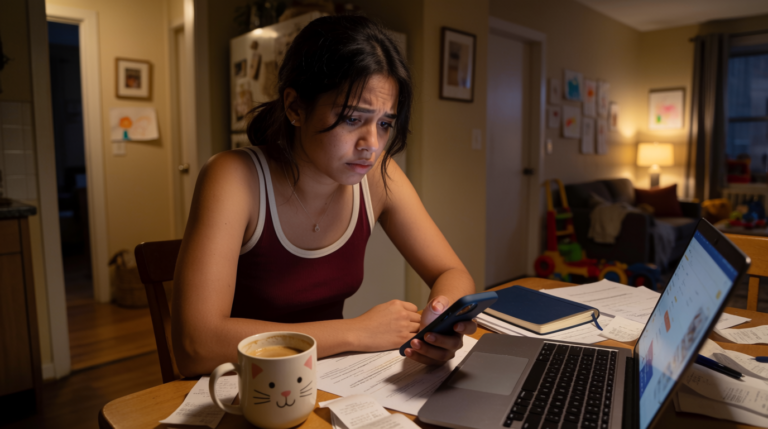

The panic hit right at the grocery checkout line. The card reader blinked twice, then declined my payment while my daughter casually asked if we could still grab ice cream. Cute timing, honestly. I had money coming in, bills mostly paid, and yet one random expense threw the whole week into chaos.

That was the moment I realized I did not actually have an emergency fund. I had optimism and caffeine. Not the same thing.

A lot of people think emergency savings only matter if you make six figures or live some ultra-organized finance influencer life with matching beige storage bins. Nope. Real life gets messy fast. Cars break down. Kids get sick. Rent increases because apparently landlords also enjoy jump scares.

The good news is you do not need a perfect budget to start. You just need a realistic plan you can actually stick to.

Here are 8 beginner-friendly emergency fund plans that work, even if money feels tight right now.

An emergency fund is not about becoming rich overnight. It is about buying yourself breathing room.

Without savings, every unexpected expense turns into stress, debt, or both. You start swiping credit cards for things that should have been annoying instead of financially devastating.

An emergency fund gives you options.

That matters more than looking successful online.

Here are a few examples:

A flash sale on skincare products? Not an emergency. Painful, yes. Emergency, no.

Takeaway: Your emergency fund protects your peace, not your shopping impulses.

If saving three to six months of expenses sounds impossible, stop there. Seriously. That giant number scares people away before they even begin.

Start with $500.

That amount can cover:

The easiest method is setting aside:

When I first started saving, I transferred tiny amounts into a separate account every Friday. Tiny. Sometimes embarrassingly tiny. But eventually it added up, which honestly felt suspicious at first 🙂

Open a savings account that is slightly annoying to access. Not impossible. Just inconvenient enough that you cannot instantly drain it for late-night online shopping.

Takeaway: Small emergency funds still count. Starting messy beats not starting at all.

This emergency fund plan focuses on building one month of living expenses first.

That means your goal is covering:

Why does this work so well for beginners?

Because one month feels reachable. Six months feels like climbing a mountain wearing flip-flops.

Try these:

As a freelancer, inconsistent income taught me this lesson fast. Some months looked amazing. Other months felt like my invoices disappeared into another dimension.

Having one month saved made slow seasons less terrifying.

Takeaway: One month of expenses can completely change how secure you feel.

This method works surprisingly well if you tend to spend emotionally. Which… honestly describes a lot of us after a stressful week.

The idea is simple:

Choose a no-spend period and move the saved money directly into your emergency fund.

You can try:

One month, I stopped buying random home decor that social media convinced me would magically fix my life. Shockingly, the beige candle holders were not the missing piece.

I saved over $300 that month alone.

Do not ban everything. That usually backfires.

Instead:

Takeaway: Temporary spending resets can kickstart your emergency savings fast.

This is probably the least exciting emergency fund plan ever created. It is also one of the most effective.

Automation removes decision fatigue.

Set up:

Even $25 weekly becomes:

That is real money.

People often wait until they feel financially ready to save. Meanwhile, financially ready usually never arrives like some magical movie scene.

Takeaway: Automation works because it removes emotion from saving.

This plan uses side income only for emergency savings.

Your regular paycheck handles normal life. Extra income builds security.

You could use:

I personally love this method because it hurts less psychologically. You are not pulling from your main budget. You are assigning bonus money a job before lifestyle creep steals it.

Because trust me, lifestyle creep is sneaky. One minute you earn extra money. The next minute you somehow own three expensive water bottles for emotional support.

Do not rely on side hustle money for survival if possible. Treat it as future protection.

Takeaway: Side hustle income can grow emergency savings surprisingly fast without squeezing your daily budget.

This approach breaks savings goals into smaller milestones.

Example:

This works well because your brain likes progress.

Huge financial goals can feel exhausting before you even start. Smaller checkpoints keep motivation alive.

Every time I hit a savings milestone, I celebrated cheaply:

Tiny rewards help. Adults also need gold stars sometimes. FYI.

Takeaway: Smaller savings milestones make long-term goals feel manageable.

Please do not keep emergency savings mixed with spending money if temptation is a problem.

Because suddenly:

A separate high-yield savings account creates mental boundaries.

Look for:

Out of sight really does help.

Rename the account something specific like:

Sounds silly. Weirdly effective.

Takeaway: Separate accounts reduce impulse spending and protect savings goals.

This emergency fund plan adjusts with your income.

Instead of fixed amounts, save:

This works especially well for:

Some months will be small. Some months bigger. The habit matters more than perfection.

Freelance income can feel wildly unpredictable. One month you feel financially responsible. The next month you are googling whether potatoes count as a complete meal.

Percentage-based saving keeps things flexible without stopping momentum.

Takeaway: Flexible savings plans work better for inconsistent income.

Most people do not magically become better savers after income increases. Expenses usually grow too.

Start with what you have now.

If your emergency fund sits beside your spending account, temptation gets loud during stressful weeks.

Create friction.

Concert tickets are not emergencies. Neither are random online sales pretending to expire in six minutes.

Use the fund carefully.

Building savings takes time. Especially during expensive seasons of life.

Slow progress still counts.

Takeaway: Consistency matters far more than speed when building an emergency fund.

A common recommendation is:

But honestly? Any savings amount is better than zero.

The goal is not perfection. The goal is stability.

Some seasons of life allow faster saving. Other seasons are about surviving daycare costs and replacing broken appliances every five minutes. Life happens.

Building an emergency fund can feel boring compared to flashy financial goals. Nobody posts dramatic social media reels about transferring $20 into savings.

But quiet financial stability changes your life in ways people rarely talk about.

You sleep better. Stress softens a little. Unexpected expenses stop feeling like personal attacks from the universe.

Start small. Stay consistent. Let the fund grow slowly in the background while you live your actual life.

Because honestly, the best emergency fund plans are not the perfect ones. They are the ones you can realistically stick with.