Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A realistic guide on how to get out of debt fast with practical habits, honest money lessons, and simple changes that actually work in normal everyday life.

The worst part about debt is not even the money.

It is the random Tuesday afternoon when your phone buzzes with another payment reminder while you are standing in the grocery store pretending to compare pasta prices. It is opening your banking app before bed and instantly regretting it. It is telling yourself next month will finally be better while quietly moving money around like a tired magician.

Most people do not end up in debt because they are reckless. Life just stacks things on top of each other. One emergency. One lazy weekend of takeout. One car repair. One medical bill. Then suddenly your paycheck already has ten jobs before it even lands in your account.

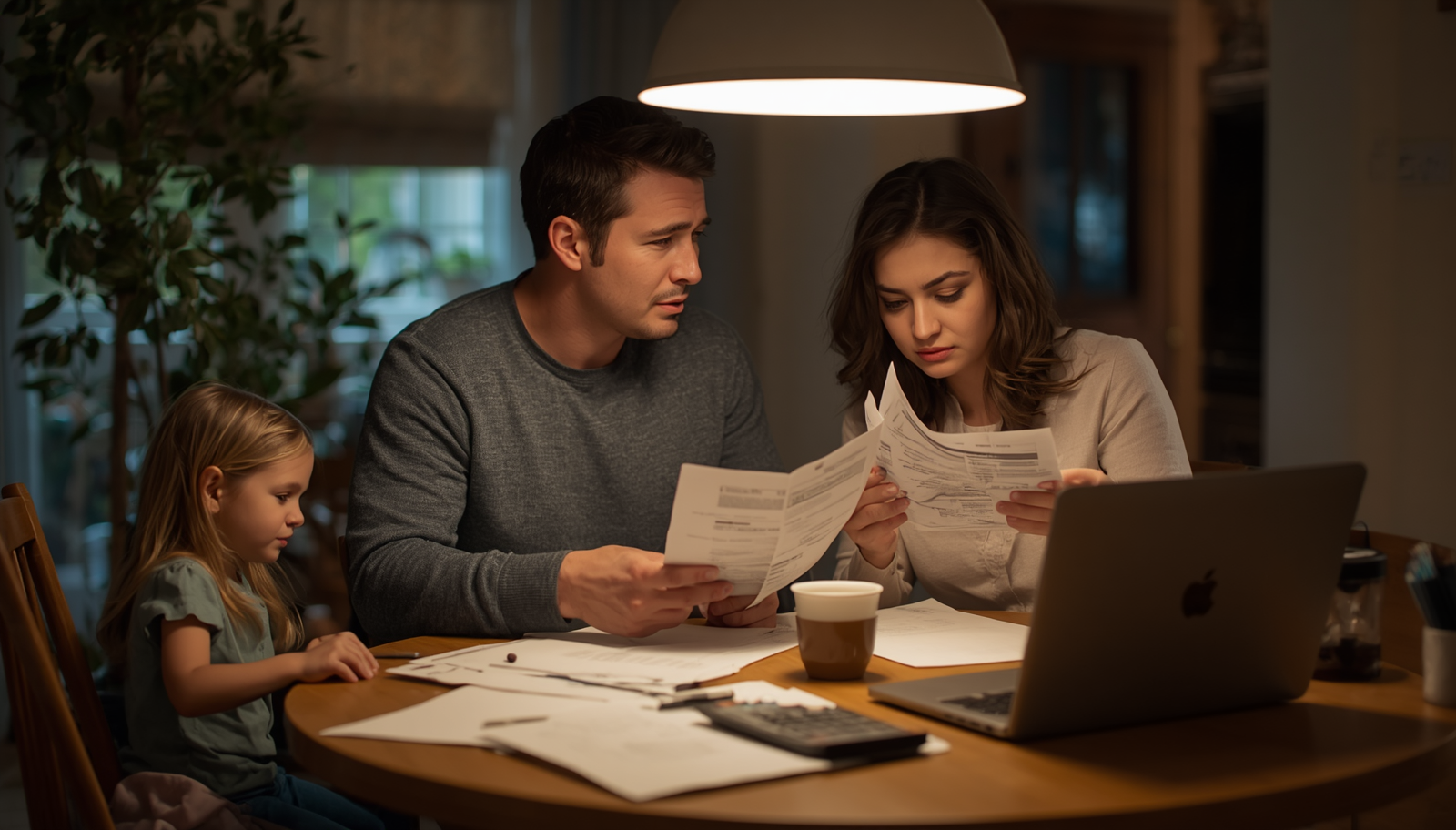

I have been there. My husband and I once sat at the kitchen table after our daughter went to sleep and realized we had been paying minimum payments for months without actually fixing anything. We looked responsible on paper. Inside? Mild panic.

The good news is this. You do not need a perfect spreadsheet, a finance degree, or a six-figure salary to start digging out. You just need realistic habits that actually fit normal life.

Here are 12 realistic ways on how to get out of debt fast without making yourself miserable.

This sounds obvious until you realize how easy it is to swipe a card for tiny stuff.

Coffee here. Fast food there. One online sale because you had a stressful day. Debt grows quietly. That is why the first step matters more than any fancy payoff method.

For one month, treat your credit cards like they are frozen in a block of ice. Literally freeze them if you need to. Use cash or debit only.

A few helpful rules:

Takeaway: You cannot get out of debt fast while still feeding the debt every week.

A lot of people avoid checking their total debt because it feels scary. I avoided it too. Weirdly enough, the uncertainty was worse than the truth.

Write down:

That is it. No fancy system required.

Seeing everything in one place gives your brain something concrete to attack. Otherwise debt becomes this giant fog monster living in the background of your life.

And FYI, most couples argue less once the numbers are actually visible. The mystery creates more stress than the spreadsheet.

People love arguing about debt strategies online. Meanwhile normal people just need something simple enough to follow after a long workday.

The two most common methods are:

Pay off the smallest balance first while making minimum payments on everything else.

This method builds motivation fast because you see quick wins.

Pay off the highest interest rate first.

This method saves more money long term.

Honestly? Both work. The best method is the one you will actually continue doing six months from now.

When we paid off one annoying store card balance, the emotional relief alone gave us momentum to keep going.

Takeaway: Consistency beats perfection every single time.

This part gets dramatic online. Suddenly everyone tells you to cancel every joy you have ever experienced.

Relax.

You do not need to live like a monk eating plain rice under candlelight.

Instead, cut the stuff you barely care about anyway.

For us, it was:

That last one hurts a little.

Look for low-pain cuts first. Those add up surprisingly fast.

Sometimes budgeting alone is not enough. Numbers are numbers.

One of the fastest ways to get out of debt is increasing income temporarily. Notice I said temporarily. You do not need to hustle 19 hours a day forever.

A few realistic ideas:

When my husband took on a few extra projects one year, every extra dollar went straight to debt instead of lifestyle upgrades. That part matters.

Otherwise the extra money disappears faster than leftover birthday cake.

People underestimate how much random money sits around their house.

Old electronics. Clothes with tags still attached. Baby gear collecting dust in the garage. That fancy kitchen appliance you used exactly once because social media convinced you homemade juice would change your life 🙂

We sold enough unused stuff one summer to knock out an entire credit card balance.

A quick tip:

Clutter and debt together create a weird mental heaviness. Clearing both feels surprisingly good.

Takeaway: Unused stuff cannot help you financially until you let it go.

This sounds backward when you already have debt. But hear me out.

Without emergency savings, every surprise expense goes right back onto a credit card. Then the cycle starts all over again.

You do not need a huge emergency fund immediately.

Start with:

That small buffer creates breathing room. It also helps you stop panicking every time life acts like life.

Because honestly, cars will still break down. Kids still get sick. Washing machines still pick the worst possible timing.

Late fees are ridiculous. They feel like getting charged extra for already struggling.

Set up automatic minimum payments at the very least.

Then use reminders for:

Debt gets worse when people avoid looking at it. Automation removes some of the emotional friction.

Also, fewer missed payments help your credit score recover faster over time.

Small systems matter more than motivation.

This one stings because social pressure is real.

People quietly go broke trying to look comfortable. Fancy dinners. Brand-name everything. Upgraded phones every year. Vacations charged to credit cards because everyone else seems to be traveling.

Meanwhile half those people are stressed too. They just post better pictures.

Some of the smartest financial decisions my family made looked boring from the outside.

We skipped upgrades. We stayed home more. We reused things longer than trends said we should. Nobody handed us a trophy, but our debt dropped.

And honestly, sleeping peacefully matters more than impressing strangers online.

Tax refunds. Bonuses. Birthday money. Side hustle payments.

It feels tempting to celebrate with a reward purchase because you finally have breathing room. I get it.

But if your goal is learning how to get out of debt fast, unexpected money can seriously speed things up.

Try this rule:

That balance helps you stay motivated without completely ignoring real life.

Financial silence creates tension fast.

One person spends. The other worries quietly. Nobody wants to start the conversation because it feels uncomfortable.

My husband and I used to avoid money talks until stress forced the issue. Once we started having short weekly check-ins, things became less emotional and more practical.

Keep it simple:

No blaming. No courtroom energy.

You are solving a shared problem, not fighting each other.

Takeaway: Debt feels heavier when couples carry it separately.

This may be the hardest truth on the list.

Getting out of debt fast usually still takes months or years. That does not mean you are failing.

People love overnight success stories online, but most real financial progress looks slow and repetitive. You make payments. You stay consistent. You keep going even when the numbers move painfully slowly.

Then one day you notice:

That change matters.

A lot.

Before you go, here are a few habits that quietly sabotage progress:

Minimum payments mostly protect the lender, not you.

Tiny spending leaks become huge over time.

People go extreme for two weeks, burn out, then quit. Slow and steady works better.

Stress shopping feels good for about twelve minutes. Then the bill arrives.

We have all been there at some point. No judgment.

Getting out of debt is rarely one dramatic moment. It is usually a hundred small decisions repeated over and over when nobody is watching.

Pack lunch more often. Skip unnecessary upgrades. Sell the unused treadmill. Pay a little extra when you can. Keep going even when progress feels boring.

That boring progress changes your life.

Because the real goal is not just becoming debt-free. The real goal is waking up without that constant financial pressure sitting in the back of your mind.

And trust me, that feeling is worth every awkward budget meeting and every skipped impulse purchase.