Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A practical and relatable guide filled with proven techniques on how to pay down debt quickly while reducing financial stress and building lasting money habits for real family life.

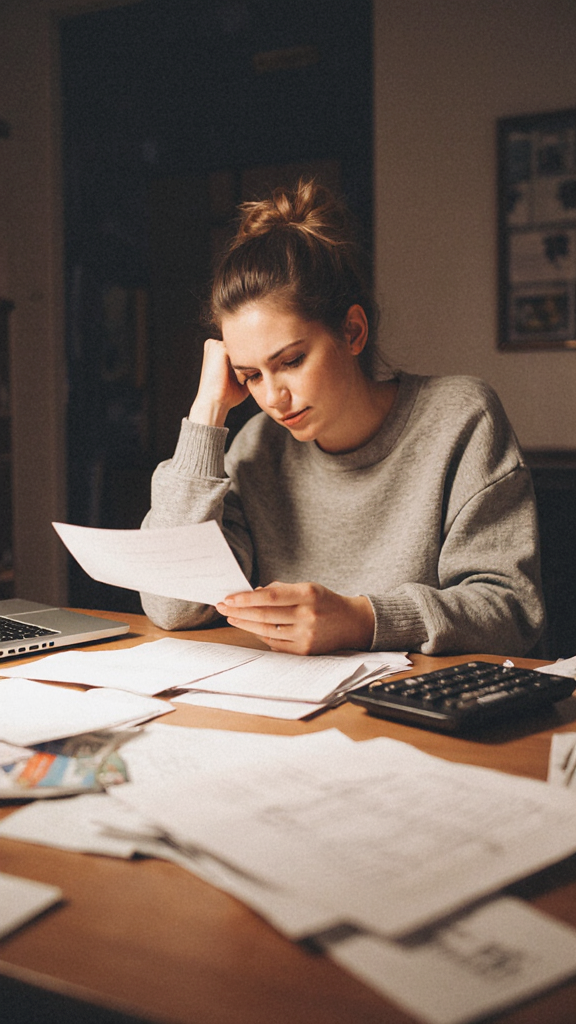

The minimum payment looked manageable right up until the interest hit again.

That cycle feels painfully familiar for a lot of people. You pay something toward the balance, feel slightly responsible for about twelve minutes, then the next statement arrives acting like your effort barely existed. Meanwhile groceries cost more, gas prices jump around emotionally, and somehow every appliance in the house decides to malfunction during the same month 🙂

That was the point where I stopped looking for perfect financial advice and started focusing on realistic ways to make actual progress.

Because honestly, learning how to pay down debt quickly is less about becoming a budgeting genius and more about building consistent habits that work during normal messy life.

These 9 proven techniques helped our family reduce debt faster without feeling completely miserable in the process.

A lot of debt advice sounds impressive but falls apart in real life.

People create extreme budgets, cut every enjoyable expense, and expect motivation to carry them forever.

Then reality appears:

The goal is not temporary perfection.

The goal is sustainable progress.

Takeaway: The best debt payoff strategies are the ones you can realistically continue during everyday life.

Trying to attack every debt equally often slows momentum emotionally.

Focusing aggressively on one balance works better for most people.

Small wins create motivation quickly.

And honestly, seeing one account disappear completely feels ridiculously satisfying :/

People stay motivated longer when progress feels obvious.

This technique feels annoying initially.

Still worth it.

Most people underestimate spending because small purchases feel harmless individually.

Then suddenly:

Tracking spending exposes financial leaks quickly.

Awareness changes spending habits faster than guilt ever will.

Takeaway: Tracking spending honestly helps identify hidden habits slowing debt payoff progress.

Convenience costs a shocking amount over time.

Delivery fees.

Takeout.

Drive-thru coffee.

Last-minute shopping.

Small conveniences slowly become expensive routines.

That does not mean eliminating every convenience forever. Sometimes survival mode wins and everyone eats frozen pizza. Real life happens FYI.

But reducing convenience spending consistently frees up extra debt payment money quickly.

Planning ahead saves more money than extreme budgeting usually does.

Large debt balances feel emotionally overwhelming.

Breaking goals into smaller pieces helps.

Instead of obsessing over total debt:

Tiny goals feel achievable.

Achievable goals create momentum.

Small progress still matters 🙂

This technique helped us more than expected honestly.

Most families own a surprising amount of unused stuff:

Apparently every household contains at least one abandoned exercise machine judging people silently from the corner.

Redirect every sale directly toward debt immediately before the money mysteriously disappears elsewhere.

Temporary spending cuts help.

Lower fixed expenses help faster long term.

Even reducing bills slightly creates monthly breathing room automatically.

A lot of recurring expenses survive simply because nobody reviews them regularly.

Takeaway: Lowering recurring monthly expenses creates automatic long-term debt payoff progress.

Extra money disappears fast without a plan.

Tax refunds.

Bonuses.

Cash gifts.

Side hustle income.

Without intention, unexpected money usually turns into random spending.

We started sending every extra dollar directly toward debt before touching anything else.

Painfully responsible behavior honestly.

The faster extra money reaches debt, the less temptation exists.

This technique feels uncomfortable but effective.

Because paying down debt while actively adding new debt feels like trying to empty a bathtub while leaving the faucet running.

We stopped using credit cards temporarily and switched to:

The adjustment felt annoying initially.

Then spending awareness improved dramatically.

Convenience often encourages overspending without people noticing.

Debt payoff becomes emotionally exhausting without encouragement.

People need occasional wins.

Not expensive rewards obviously. That defeats the purpose completely.

Simple affordable rewards work best:

Tiny rewards make difficult habits sustainable IMO.

Financial goals should feel challenging, not emotionally miserable.

Takeaway: Sustainable debt payoff plans include realistic encouragement and emotional balance.

Even motivated people accidentally sabotage progress sometimes.

Extreme restriction rarely lasts.

Stress affects financial choices constantly.

Unexpected expenses happen to everyone.

Ignoring balances never improves them unfortunately :/

Consistency matters more than perfection.

Honestly, the biggest shift was emotional.

Before getting serious about debt payoff, money conversations felt stressful constantly. Every unexpected expense triggered anxiety immediately.

Eventually we started noticing changes:

Not overnight.

But steadily.

And honestly, steady progress feels far more realistic than dramatic overnight success stories online.

Motivation disappears sometimes.

That is normal.

A few things helped us continue:

Because debt payoff is not only about money.

It is about:

Those things matter deeply.

These 9 proven techniques on how to pay down debt quickly work because they focus on realistic consistent progress instead of financial perfection.

Debt payoff does require discipline.

But it also requires patience, emotional awareness, and systems that fit actual everyday life.

Start smaller than you think.

Stay consistent longer than you expect.

Celebrate progress more often than you usually would.

Because honestly, most people reach financial freedom through ordinary repeated habits, not dramatic life transformations.

One payment.

One better choice.

One less stressful month at a time.