Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A simple, honest plan to pay off debt within a year without burning out, built for real life, real budgets, and real families.

The credit card bill sat open on my laptop while my daughter asked for snacks in the background. Numbers stacked on top of numbers, and somehow none of them looked small. I kept telling myself I had time. Then I did the math and realized time was exactly what I was running out of.

That moment felt familiar in a way I did not like. Too many of us live in that quiet stress where debt just hangs around like an uninvited guest. You keep working, keep paying, but it never really leaves.

So I stopped guessing and built a plan. Not a perfect one. Just one that actually worked in real life.

Here are the 6 steps to ensure all my debts are paid in full by next year, without losing my sanity in the process.

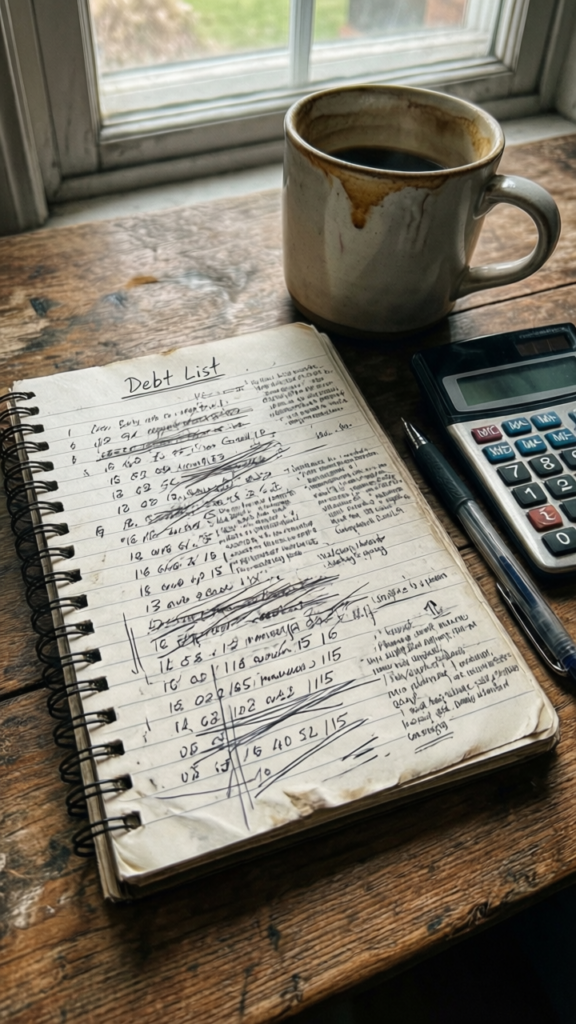

I used to avoid looking at all my debts at once. It felt safer to check one account at a time and pretend the rest did not exist. That strategy worked… until it didn’t.

Sit down and list everything:

Write down:

No guessing. No rounding down to feel better.

The first time I did this, I felt a bit sick. But something shifted too. When everything sat in one place, it stopped being this vague, scary cloud.

Takeaway: You cannot fix what you refuse to fully see. Clarity beats comfort every time.

There are two common ways to attack debt:

Pay off the smallest debt first. Then roll that payment into the next one.

Pay off the highest interest rate first to save more money long term.

I tried the logical route first. Avalanche made sense on paper. But honestly, it felt slow and boring. I needed quick wins or I would quit halfway through.

So I switched to snowball.

Paying off one small card gave me momentum. It felt like progress, not punishment.

Ask yourself:

There is no perfect method. Only the one you will actually stick to.

Takeaway: The best plan is the one you will not abandon after two weeks.

Next year sounds nice, but it is too vague. I needed a real number.

So I worked backward:

Was it uncomfortable? Yes. Did it force me to get serious? Also yes.

I realized my usual payments were not enough. I had to stretch a bit. Not to the point of burnout, but enough to feel it.

Think of it like this. If your plan feels too easy, it probably will not change much.

Takeaway: A clear deadline turns a wish into a commitment.

I hate extreme budgeting. Cutting everything fun out of life just makes me rebel later. And then I spend more. Classic.

Instead, I looked for realistic cuts:

I kept a few things that made life feel normal. Coffee runs stayed. Small treats stayed. Because I know myself.

This is not about punishment. It is about control.

Also, I involved my family. Even my daughter understood simple changes like eating at home more often. It became a team effort instead of a secret struggle.

Takeaway: Sustainable cuts beat extreme cuts that you cannot maintain.

There is a limit to how much you can cut. At some point, you need to bring in more.

As a freelancer, I had options:

None of this felt huge on its own. But together, it made a real difference.

Even an extra few hundred a month can speed things up more than you think.

If freelancing is not your thing, consider:

It does not have to be forever. Just long enough to hit your goal.

Takeaway: More income gives you breathing room and faster results.

At first, I avoided checking my balances. It stressed me out. But ignoring it made things worse.

So I started tracking weekly.

Not daily. That gets obsessive. But weekly felt right.

I used a simple tracker:

Watching the numbers drop became weirdly satisfying. Like a game I actually wanted to win.

And on tough weeks, it reminded me that progress was still happening, even if it felt slow.

Also, celebrate small wins. Paid off one card? That deserves a quiet happy dance in your kitchen. FYI, those moments keep you going.

Takeaway: What you track improves. Progress becomes real when you can see it.

Let me save you some frustration.

I made all of these mistakes. More than once. 🙂

It was not just about money.

I slept better. I stopped avoiding emails. I felt more present with my family instead of constantly worrying in the background.

And something else happened. I stopped feeling ashamed.

Debt used to feel like a personal failure. Now it feels like a problem I am actively solving.

That shift matters more than any spreadsheet.

Paying off debt in a year is not easy. It takes effort, honesty, and a bit of stubbornness. But it is doable when you stop guessing and start acting with intention.

If you take anything from this, let it be this:

You do not need a perfect plan. You need a consistent one.

Start messy. Adjust as you go. Keep showing up, even when it feels slow. Because one day, you will open that same laptop, check your balances, and realize the numbers no longer control you.

And that feeling is worth every bit of effort.