Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A simple, honest breakdown of how to build a debt payoff plan that actually works without burnout, guilt, or unrealistic budgeting.

The credit card bill sat open on the table while dinner got cold. I kept doing the math in my head like it would magically shrink. It didn’t. My husband asked if everything was okay, and I gave the classic fine answer while mentally calculating interest like a stressed-out accountant 🙂

That moment felt painfully normal. Too normal. If you’ve ever shifted money around hoping it buys you peace, you’re not alone. Debt has a sneaky way of turning smart people into avoiders.

Here’s the thing. A real debt payoff plan that actually works isn’t about being perfect. It’s about being honest, a little stubborn, and surprisingly practical.

Let’s walk through five proven steps that helped me go from overwhelmed to in control.

Avoiding your debt doesn’t make it smaller. It just makes it louder in your head.

I used to check one balance at a time like I was rationing bad news. Big mistake. The turning point came when I sat down and listed every single debt in one place. Credit cards, personal loan, the random buy now pay later thing I forgot about. All of it.

Yes, this part feels awful. Do it anyway.

When you see everything together, something shifts. It goes from vague panic to a real problem with edges. And real problems can be solved.

Takeaway: Clarity kills anxiety. You can’t fix what you won’t face.

People love arguing about the best method. Snowball or avalanche. Math or motivation. Here’s my honest take. The best strategy is the one you won’t quit after two weeks.

Debt Snowball

Debt Avalanche

I started with avalanche because it made sense on paper. Then I got bored. Progress felt invisible. So I switched to snowball and suddenly I was obsessed with knocking out accounts.

Was it perfectly optimized? Nope. Did it work? Yes.

Sometimes you need momentum more than perfection.

Takeaway: Choose the method that keeps you consistent, not the one that looks smartest.

If your budget makes you miserable, you won’t follow it. It’s that simple.

I tried the ultra strict version once. No coffee, no takeout, no fun. I lasted eight days. Then I stress spent twice as much. Classic.

A working budget should feel like structure, not a prison.

I call this the sane budget. It leaves room for real life. Kids get sick. Work gets stressful. Sometimes you just want dessert without guilt.

Also, include a mini buffer. Even 20 dollars helps you avoid putting surprise expenses back on credit.

Takeaway: A good budget supports your life. It doesn’t fight it.

Cutting expenses helps. But there’s a limit. You can only cut so much before life gets depressing.

Earning more gives you breathing room and speeds things up.

I started small. Freelance writing after my daughter went to bed. Nothing fancy. Just consistent. That extra income went straight to debt.

You don’t need a full career shift. You need a temporary boost.

And no, you don’t need to hustle 24 hours a day. That’s a fast track to burnout. Keep it manageable. Even an extra 100 to 300 a month makes a real difference.

Takeaway: More income creates faster results and less stress. Keep it simple and sustainable.

Motivation is unreliable. It shows up strong at the beginning, then disappears when things get boring.

And debt payoff gets boring. There’s no way around it.

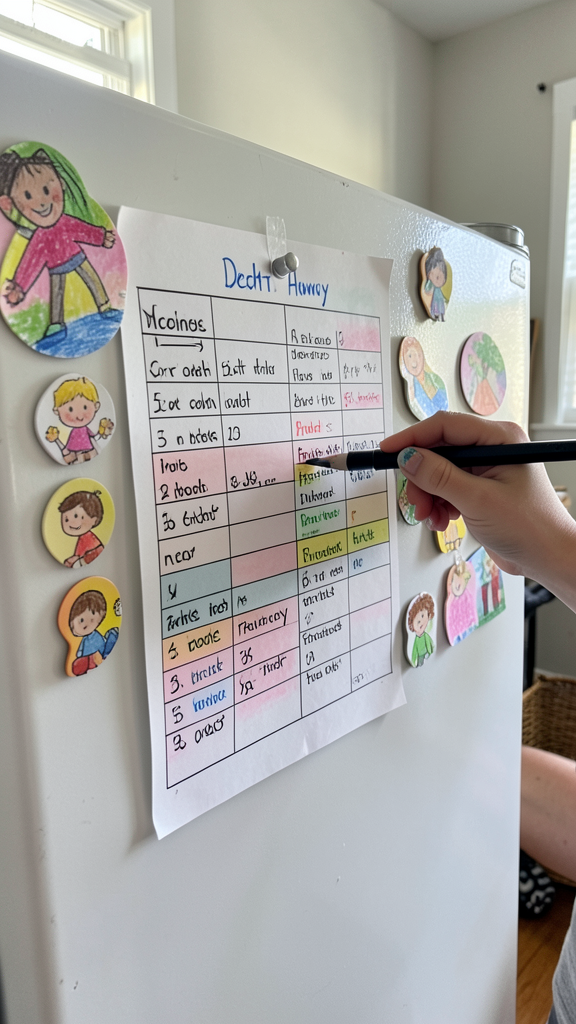

The trick is to build systems that carry you through low energy days.

I used a simple chart on the fridge. Every time we paid off a chunk, I colored it in. My daughter thought it was a game. Honestly, so did I 🙂

Also, expect setbacks. They will happen. Car repairs, medical bills, random life chaos. The goal isn’t perfection. It’s getting back on track quickly.

Takeaway: Consistency beats intensity every time. Keep going even when it feels slow.

Let’s talk about the stuff that looks harmless but can derail everything.

Paying randomly without a strategy costs you more over time. Always have a plan.

This can hurt your credit score. Pay them off first, then decide what to do.

Even a small one matters. Without it, every surprise goes back on debt.

Missing one payment or overspending one week doesn’t mean you failed. It means you’re human.

Takeaway: Avoiding these small mistakes can save you months of effort.

It’s not glamorous. It’s not fast. And it’s definitely not linear.

Some months you’ll feel unstoppable. Other months you’ll question everything. You’ll wonder if it’s even worth it.

Then one day, a balance hits zero.

And it feels… quiet. Not fireworks. Just relief. Like you finally have space to breathe again.

That’s the real reward.

This is the question everyone asks.

The honest answer depends on your numbers, your income, and your consistency. But here’s a rough idea.

Focus less on the timeline and more on progress. Progress compounds.

Takeaway: Speed matters less than direction. Moving forward is what counts.

A debt payoff plan that actually works isn’t complicated. It’s just uncomfortable at first.

You face the numbers. You pick a strategy. You build a realistic budget. You earn a little more. And you stay consistent longer than you thought you could.

That’s it.

If you’re waiting to feel ready, you might be waiting forever. Start messy. Start small. Just start.

Because the sooner you begin, the sooner you get your peace back 🙂