Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

These smart strategies for budgeting for debt repayment can help families reduce financial stress, stay consistent with money goals, and finally make real progress toward debt freedom.

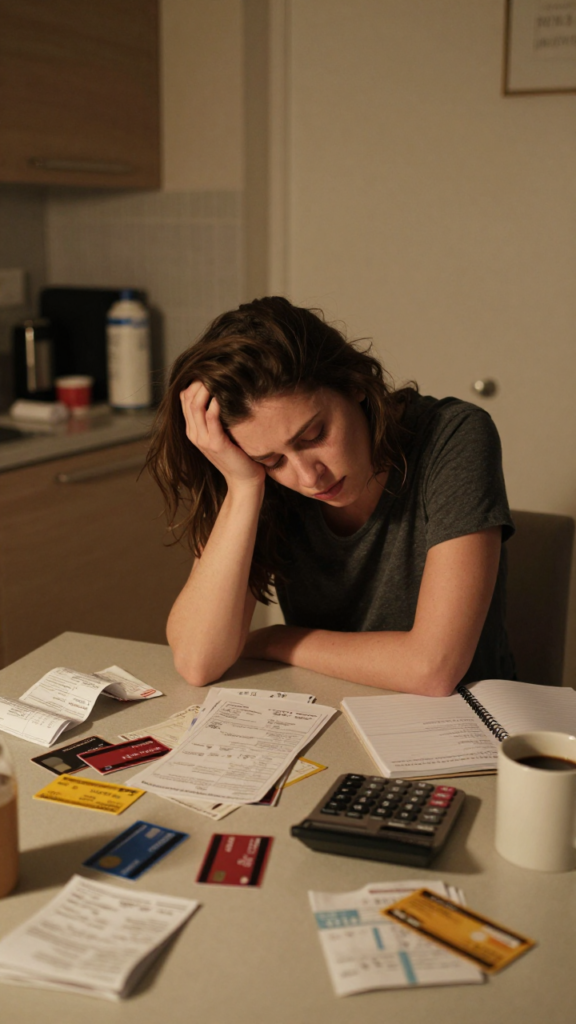

The credit card bill sat on the counter beside a half-drunk coffee and a grocery receipt that somehow reached a number usually reserved for small medical procedures.

I kept opening the budgeting app, closing it, then pretending future me would magically become more organized.

Funny how debt repayment always sounds simple until real life shows up with school expenses, rising groceries, and a random car noise that immediately costs four hundred dollars.

Still, budgeting for debt repayment changed everything for our family once we stopped treating it like punishment.

A good budget does not exist to make life miserable. It exists to stop financial chaos from running the household.

These 12 smart strategies for budgeting for debt repayment helped us reduce stress, stay consistent, and finally feel like we were making real progress instead of just financially jogging in place.

Most people fail at debt budgets for one reason.

They create fantasy budgets.

Fantasy budgets assume:

Real budgets need flexibility.

Otherwise people quit within two weeks and order takeout out of frustration.

Takeaway: The best debt repayment budget is realistic enough to survive normal life problems.

This sounds obvious until people avoid checking balances for six months straight.

I did that once.

Terrible strategy honestly.

Write down:

No guessing.

Real numbers matter because vague financial stress feels bigger than reality most of the time.

Clarity reduces anxiety.

Your brain stops imagining catastrophic numbers once you finally face the situation directly.

A bare bones budget focuses only on essentials temporarily.

That includes:

Not weekly shopping trips disguised as emotional support.

That one hurts slightly FYI.

We cut several small expenses for six months:

Nothing dramatic.

Just enough to free extra debt payoff money.

Money disappears fast without direction.

Every paycheck needs assignments before spending begins.

Try categories like:

Otherwise money wanders away like an unsupervised toddler near crayons.

Intentional spending creates awareness automatically.

People spend differently once every dollar already has a purpose.

Takeaway: Assigning every dollar intentionally helps prevent emotional and accidental overspending.

This step saved us repeatedly.

Without emergency savings, every unexpected expense goes directly onto credit cards again.

That cycle becomes exhausting fast.

Aim for:

Even small emergency funds create breathing room.

Our washing machine broke during debt payoff.

Without emergency savings, we would have added more debt immediately.

Instead, we paid cash and moved on.

Still annoying though 🙂

Both methods work.

The best one is honestly the one you will continue doing consistently.

Pay smallest balances first for motivation.

Pay highest interest rates first to save money.

We used a hybrid approach because apparently I enjoy making budgeting systems more complicated than necessary.

Debt repayment takes time.

Small wins help people stay emotionally committed.

Some budgeting advice acts like families should survive entirely on dry beans forever.

That gets old fast.

Instead:

Small grocery improvements matter hugely over time.

Repeating simple meals reduced stress and spending dramatically.

Fancy meal planning overwhelmed me honestly.

Ignoring finances does not improve finances.

Unfortunately.

Weekly budget reviews help catch problems early before spending spirals completely.

Keep it short:

My husband and I started doing budget check ins Sunday evenings after our daughter went to bed.

Way less stressful than fighting about money unexpectedly midweek.

Certain spending categories become dangerous quickly.

For many people:

Cash creates physical awareness.

Swiping cards feels emotionally invisible sometimes.

People naturally spend less when physically handing over money.

Behavior changes when spending feels tangible IMO.

Takeaway: Cash systems can reduce overspending by increasing awareness and slowing impulsive purchases.

Cutting expenses helps.

Increasing income helps faster.

Debt repayment speeds up dramatically with:

During one rough season, I sold old furniture and took extra freelance work after bedtime.

Not glamorous.

Very effective.

Temporary sacrifice works better when it stays temporary.

Burnout helps nobody.

This one changed my mindset deeply.

A lot of spending comes from image maintenance:

Debt freedom often requires becoming comfortable looking normal.

Honestly, normal became peaceful after a while.

The people judging your older car usually are not paying your credit card bills anyway.

People quit debt repayment when life feels joyless.

Celebrate milestones simply:

Reward progress carefully without undoing it financially.

We made homemade pizza and watched movies every time we paid off a debt.

Simple traditions matter more than expensive rewards sometimes.

Perfection destroys consistency.

Some months will go badly.

Unexpected expenses happen.

Motivation disappears occasionally.

That does not mean the plan failed.

Debt repayment succeeds through steady imperfect progress over time.

Financial improvement looks messy in real life.

Nobody maintains perfect discipline constantly.

A few mistakes slow progress quickly.

Tiny spending leaks add up surprisingly fast.

People forget:

Then budgets collapse suddenly.

Extreme restriction usually backfires eventually.

Sustainable budgets matter more than aggressive unrealistic ones.

Takeaway: Flexible realistic budgets last longer and create better long-term debt repayment success.

The money stress did not disappear overnight.

But the chaos slowly decreased.

We stopped panicking constantly before checking bank balances.

We argued less.

We planned more intentionally.

And honestly, the emotional relief mattered almost more than the financial progress.

That surprised me.

Budgeting gave us clarity.

Clarity gave us peace.

These 12 smart strategies for budgeting for debt repayment work because they focus on realistic habits instead of financial perfection.

Start small.

Stay consistent.

Adjust when necessary.

A solid debt repayment budget should support your life, not punish it.

Because at the end of the day, financial freedom is not really about spreadsheets.

It is about finally feeling calm when you open your banking app instead of preparing emotionally for bad news.