Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A real-life, no-fluff guide to breaking free from credit card debt using simple, practical habits that actually stick.

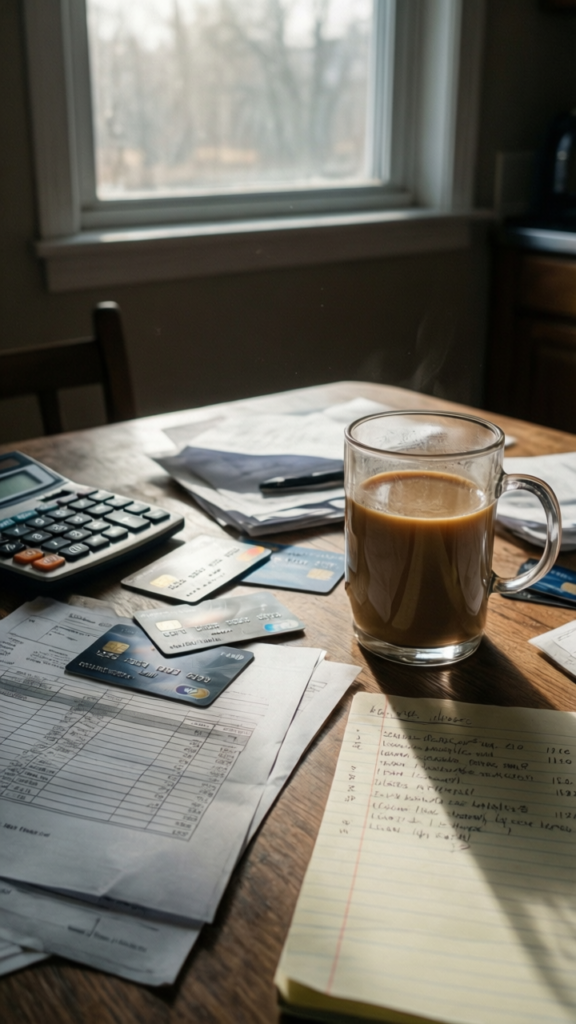

The notification popped up again. Another minimum payment due. Another quiet promise to deal with it later. Meanwhile, groceries got pricier, the kid needed new shoes, and somehow that balance never moved. Sound familiar?

That slow, sticky feeling of credit card debt is something most of us carry at some point. Not dramatic, not catastrophic. Just… always there. And honestly, it gets exhausting.

So let’s talk about the 12 best way to pay off credit cards for good in a real-life, no-nonsense way. No fluff. No magical thinking. Just what actually works when you’re juggling bills, work, and a family.

I avoided this step longer than I want to admit. Because opening all those statements felt like opening a horror movie.

But here’s the truth. You can’t fix what you refuse to look at.

Start by listing:

Put it somewhere visible. Yes, even the ugly numbers.

Takeaway: Clarity beats anxiety every single time.

There’s no perfect method. Only the one you’ll actually stick to.

I went with snowball because I needed motivation more than math. Watching one card disappear felt like winning something.

Takeaway: The best method is the one you won’t quit after two weeks.

This sounds obvious. It’s not.

I used to justify small swipes. It’s just coffee. It’s just a quick online order. Suddenly, it wasn’t small anymore.

Try this:

FYI, convenience is expensive when you’re in debt 🙂

Takeaway: You can’t drain a tub while the faucet is still running.

Not a fancy spreadsheet. Just a simple plan.

Break it down:

Then trim the fluff. Not forever. Just for now.

I cut back on random takeout and subscription apps I barely used. Turns out I didn’t need five streaming services.

Takeaway: A simple budget creates space for progress.

Discipline is great. Automation is better.

Set up:

This removes the mental load. No more forgetting. No more late fees.

Takeaway: Make your system do the work when your motivation disappears.

Everyone says earn more. Sure, but let’s be realistic.

Here are doable options:

I sold an old camera and a pile of things I forgot I owned. That alone knocked out a chunk of debt.

IMO, quick wins like this matter more than perfect plans.

Takeaway: Small bursts of extra cash can speed things up fast.

This feels awkward, but it works more often than you think.

Call your credit card company and ask:

Worst case, they say no. Best case, you save hundreds.

Takeaway: Asking costs nothing and can pay off big.

This one can help or hurt.

A balance transfer card with 0 percent interest can give breathing room. But only if you stay disciplined.

Watch out for:

I used this once and it helped, but I treated it like a strict deadline.

Takeaway: Tools work only when your habits support them.

Tax refund. Bonus. Cash gifts.

The old me would split it between fun and bills. The current me sends most of it straight to debt.

Not exciting, I know. But very effective.

Takeaway: One smart decision with a lump sum can save months of effort.

Because it does.

I kept a simple tracker:

Seeing progress kept me going when things felt slow.

There’s something oddly satisfying about watching numbers shrink.

Takeaway: Progress you can see is progress you’ll continue.

This sounds backward when you have debt. But hear me out.

Without a cushion, every unexpected expense goes back on your card.

Start small:

That little buffer saved me more than once.

Takeaway: A safety net prevents debt from creeping back in.

This is the hardest part. And the most important.

Paying off debt is not just math. It’s behavior.

Ask yourself:

I had to admit I used shopping as a reward after long days. Once I noticed it, I replaced it with cheaper habits. Walks, journaling, even just scrolling without buying anything :/

Not glamorous, but it worked.

Takeaway: Lasting change happens when your habits change, not just your balance.

Paying off credit cards for good is not about one big move. It’s about a hundred small, consistent ones that add up over time.

Some months will feel easy. Others will feel like nothing is moving. That’s normal. Keep going anyway.

Because one day, you check your balance and realize it’s gone. No drama. No big moment. Just quiet relief.

And honestly, that feeling is worth every bit of effort.