Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Credit card debt feels overwhelming until you build a realistic payoff plan that actually fits real life, messy moments and all.

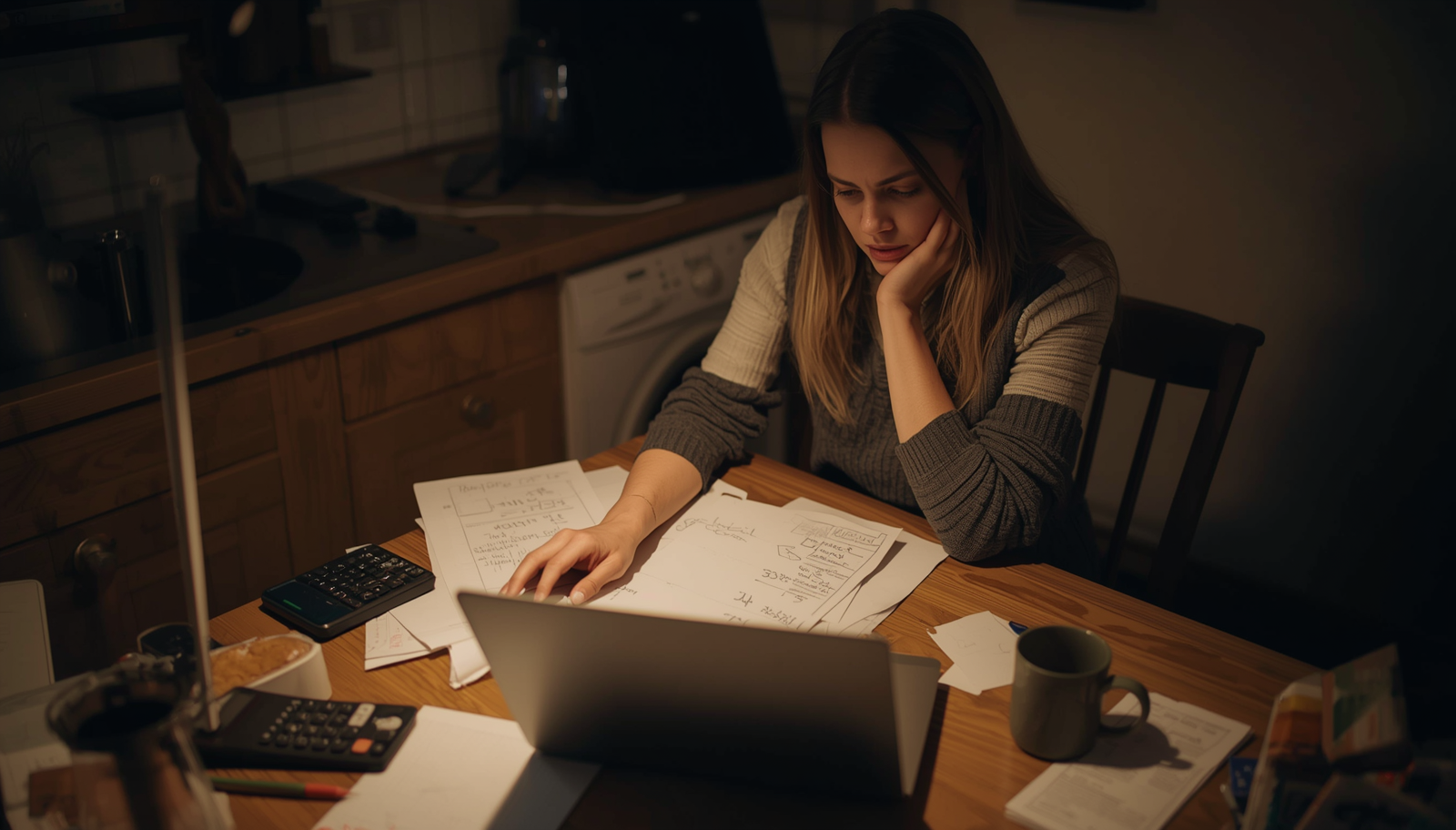

The moment usually hits at night.

You check your banking app, half-hoping the numbers somehow fixed themselves while you were busy living your life. They did not. Your credit card balance still sits there like an unwanted houseguest, eating snacks and refusing to leave.

If that sounds familiar, welcome. You are in crowded company.

Credit card debt has a sneaky way of piling up. It rarely starts with reckless spending. More often, it starts with groceries, a car repair, a birthday gift, or one too many takeout nights because life got chaotic. Then suddenly you are paying interest on top of interest and wondering how your card became your least favorite monthly subscription.

Been there. As a business owner, freelancer, wife, and mom, I have had months where cash flow looked more like a toddler finger painting than a proper budget. I learned the hard way that paying off debt is less about math and more about behavior.

The good news? You do not need magic. You need a plan.

Here are 10 proven strategies for your credit card debt payoff that actually work.

Avoidance feels safer. It also keeps you stuck.

The first time I wrote down every credit card balance, interest rate, and minimum payment, I wanted to throw the notebook across the room. It was ugly. But ugly numbers beat invisible numbers every time.

Make a simple list:

That is it. No fancy spreadsheet required unless spreadsheets bring you joy. Weird hobby, but okay 🙂

Takeaway: You cannot fix what you refuse to look at.

This sounds obvious. It also sounds rude.

But if you keep swiping while trying to pay off debt, you are basically trying to dry the floor while the sink is still overflowing.

A few practical ways to stop:

I once deleted my card from every online store after buying throw pillows I absolutely did not need. Decorative debt is still debt.

Takeaway: Your payoff plan starts with stopping the leak.

People love debating this one. It is almost a personality test.

There are two popular methods.

Pay off the smallest balance first while making minimum payments on everything else.

Why it works:

I love this method because humans are emotional creatures pretending to be logical.

Pay off the highest interest rate first.

Why it works:

IMO, choose the method that keeps you moving. The perfect plan you quit is worse than the imperfect plan you finish.

Takeaway: Pick one method and stop overthinking it.

Not forever. Relax.

A temporary budget means cutting hard for a season so future-you can breathe easier.

Ask yourself:

For three months, my family cut:

Yes, it hurt a little. No, we did not perish.

That money went straight to debt.

Takeaway: Short-term discomfort creates long-term freedom.

Minimum payments are a trap.

They keep your account current while quietly extending your debt into the next century. Slight exaggeration, but not by much.

Set up automatic payments above the minimum. Even an extra $50 matters.

For example:

That extra $50 chips away at principal faster than you think.

FYI, automation removes decision fatigue. Your tired brain cannot sabotage what it never has to decide.

Takeaway: Automation turns good intentions into actual progress.

This part matters more than most people admit.

Cutting expenses has limits. Income has more upside.

As a freelancer, this became my favorite debt weapon. I took on extra client work specifically for debt payoff. Not forever. Just long enough to move the needle.

Ideas:

Then do something radical.

Send all extra income directly to debt.

Not half. Not most. All.

Yes, even that side hustle money from selling your old treadmill that became an expensive clothes rack.

Takeaway: Temporary hustle can create permanent relief.

Nobody wants to do this. Do it anyway.

Call and ask:

The worst they say is no.

Years ago, one five-minute phone call dropped my interest rate by several points. I felt mildly offended that they agreed so easily. Like, you could have done this the whole time?

Takeaway: A simple phone call can save hundreds.

A balance transfer card can help if used wisely.

Keyword: wisely.

A 0 percent intro APR can buy breathing room. But only if you aggressively pay it down before the promotional period ends.

Check:

Do not treat this like a fresh start to spend more. That is how people accidentally create sequel debt. Nobody asked for that.

Takeaway: Balance transfers work best with a strict payoff deadline.

This sounds backward, but hear me out.

Without savings, every surprise becomes new debt.

Your tire blows out.

Your kid gets sick.

Your fridge makes that weird noise.

Boom. Credit card again.

Start small:

That tiny buffer protects your progress.

As a mom, this changed everything for me. Debt payoff stopped feeling fragile.

Takeaway: A small emergency fund prevents repeat debt.

Because they do.

Paying off debt can feel slow. You need proof that progress is happening.

Try:

My family literally cheered when one card hit zero. Was it dramatic? Absolutely. Was it effective? Also yes.

Progress deserves attention.

Takeaway: What gets tracked gets finished.

Even smart people do these.

Consistency beats motivation every time.

Those little percentages are not little.

You will mess up. Budgeting is messy. Real life is messy.

One bad month does not erase your plan.

Talk to your spouse or accountability partner.

When my husband and I started having honest money conversations, our progress sped up fast. Shame loves silence. Progress loves visibility.

Takeaway: Mistakes happen. Quitting is the real problem.

Yes, less debt.

But also:

That part surprised me most.

Debt payoff is not just financial. It is emotional.

When you stop owing everyone, you start feeling like yourself again.

And that feels really good.

Simple? Yes.

Easy? Not always.

Worth it? Absolutely.

Your credit card debt did not appear overnight, and it will not disappear overnight either.

That is okay.

You do not need a perfect month. You need your next good decision.

Make that one today.

Then make another tomorrow.

That is how debt disappears. Not through motivation. Through boring, stubborn consistency. And honestly, boring has never looked so beautiful.