Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

A practical and relatable step-by-step guide on how to pay off 5000 in debt using realistic budgeting habits, emotional motivation, and sustainable financial strategies for everyday family life.

The number sat there on the phone screen while I stood in the kitchen pretending to listen to my daughter ask for snacks.

Five thousand dollars.

Not fifty thousand. Not life-destroying levels of debt. But still enough to make my stomach tighten every time another payment notification appeared. Enough to make normal grocery trips feel stressful. Enough to quietly sit in the background of every financial decision.

That is the weird thing about debt.

Even smaller balances can feel emotionally exhausting when money already feels tight.

For a while, I kept telling myself I would deal with it later. Later when work improved. Later when expenses slowed down. Later when life magically became cheaper. Spoiler alert. Life never volunteered to become cheaper 🙂

Eventually I realized I needed an actual plan.

Not vague motivation. Not random budgeting attempts. A real step-by-step system.

If you are trying to figure out how to pay off 5000 in debt, this guide will help you create realistic momentum without turning your life into financial punishment.

People sometimes minimize smaller debt amounts.

But honestly, 5000 dollars can feel huge when:

The emotional weight matters too.

Debt affects:

That is why paying it off matters beyond the numbers.

Takeaway: Even moderate debt can create major emotional stress when life already feels financially overwhelming.

This step feels terrible initially.

Do it anyway.

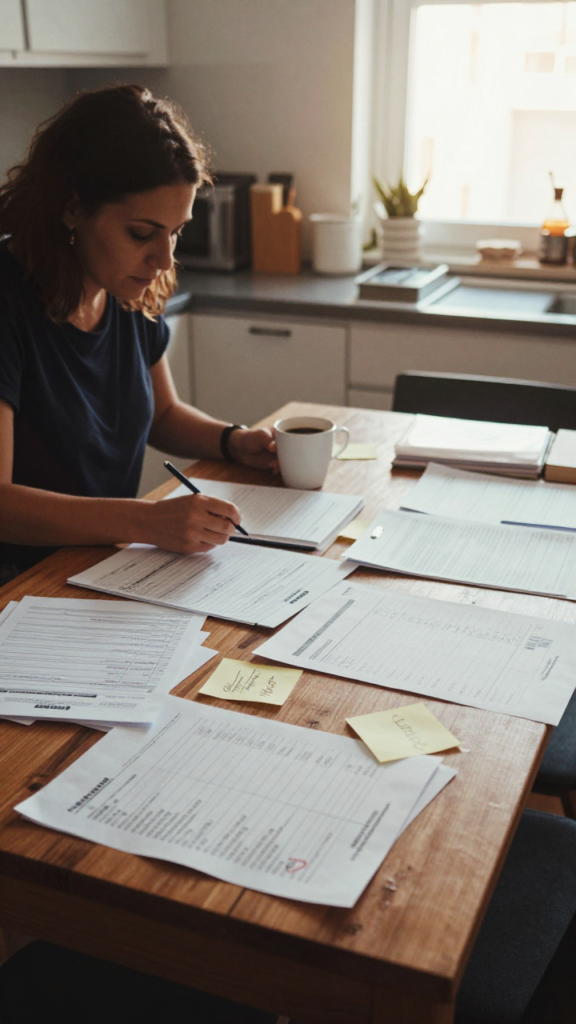

A lot of people avoid checking balances because seeing the numbers creates anxiety. I understand completely. For months I mentally rounded balances instead of actually looking at them directly. Apparently vague panic felt more manageable than math FYI.

But clarity matters.

Write down:

Seeing everything in one place immediately reduces some mental chaos.

| Debt Type | Balance | Minimum Payment | Interest Rate |

|---|---|---|---|

| Credit Card A | $2,200 | $65 | 24% |

| Credit Card B | $1,300 | $40 | 19% |

| Personal Loan | $1,500 | $75 | 11% |

Suddenly the situation feels measurable instead of emotionally foggy.

You do not need a perfect color-coded spreadsheet.

You just need honesty.

A temporary bare-bones budget helps free up extra money for debt payoff.

Focus only on essentials:

Then reduce unnecessary spending temporarily.

Not forever.

Just long enough to create momentum.

Honestly, Target trips alone probably deserve their own financial recovery program :/

Takeaway: Temporary spending cuts create faster debt payoff momentum without requiring permanent misery.

This part matters because random payments slow progress.

Most people choose between:

Pay smallest balances first.

Benefits:

Pay highest interest rates first.

Benefits:

Personally, I preferred the snowball method because small wins kept me emotionally motivated.

And honestly, motivation matters a lot during debt payoff.

People immediately think they need three side hustles and permanent exhaustion.

Sometimes extra income helps. But smaller changes add up too.

Start by finding realistic extra money monthly.

Even an extra 200 dollars monthly changes payoff speed dramatically.

If you pay:

Small consistent amounts matter more than occasional giant payments.

Late fees make debt worse quickly.

Automating minimum payments protects you from:

Then manually send extra payments toward your target debt.

This system reduced so much stress in our house honestly.

Because remembering fifteen financial details constantly becomes exhausting after a while.

Takeaway: Automation reduces mistakes and helps debt payoff stay consistent during busy stressful seasons.

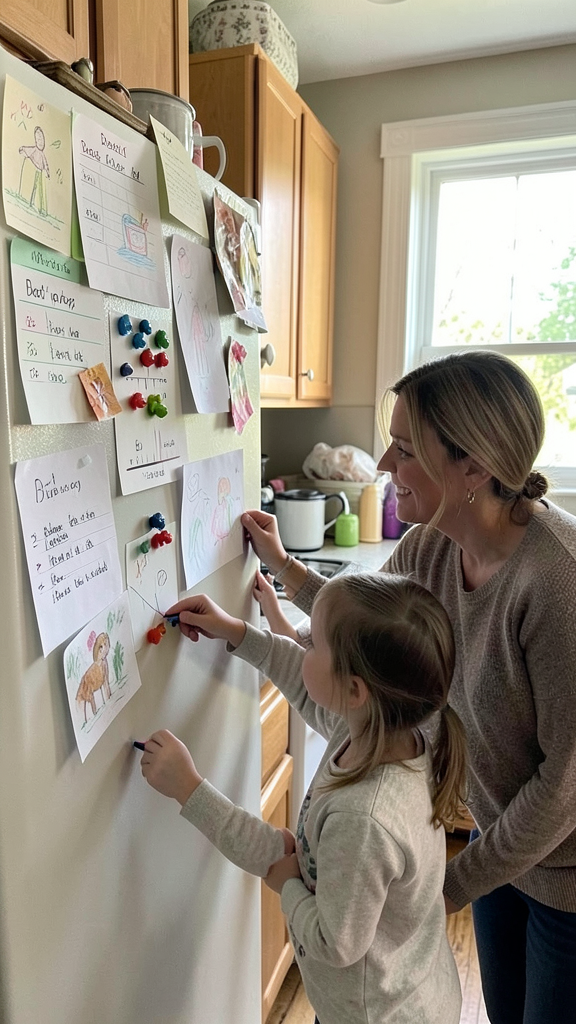

This sounds silly until you try it.

Visual progress tracking genuinely helps motivation.

Use:

Coloring in progress sections feels weirdly satisfying.

My daughter used to cheer every time we crossed out another balance, which somehow made debt payoff feel slightly less depressing 🙂

The brain likes visible rewards.

This part matters more than people expect.

Paying off debt while creating new debt feels emotionally exhausting.

Focus on:

Not perfection.

Just awareness.

That final question stopped many questionable online purchases for me IMO.

One surprise expense can derail progress fast.

That is why small emergency savings matter even during debt payoff.

Start small if necessary:

Because without emergency savings, every unexpected expense returns straight to credit cards.

And nobody enjoys financial progress repeatedly getting body-slammed by car repairs.

Takeaway: Small emergency savings help protect debt payoff progress from unexpected setbacks.

Debt payoff takes time.

Without encouragement, burnout happens quickly.

Small rewards help maintain motivation:

The goal is balance.

Not turning life into endless financial punishment.

Simple pleasures matter during stressful financial seasons.

This mindset shift changed everything for me.

A lot of people obsess over paying debt off immediately. Then they burn out after one difficult month.

Slow progress still counts.

Seriously.

Consistent payments matter more than dramatic temporary intensity.

Boring consistency creates real results.

Not motivational panic.

A few habits slow progress unnecessarily.

Stress affects spending constantly.

Overly restrictive budgets often fail quickly.

Financial avoidance increases anxiety long term.

Your timeline does not need to match social media debt payoff stories.

Real life varies.

Takeaway: Sustainable debt payoff habits work better than extreme short-term financial pressure.

Honestly, the biggest change was not financial at first.

It was emotional relief.

As balances dropped:

Not perfect.

Just less heavy.

And that emotional breathing room mattered more than I expected.

Five thousand dollars of debt can feel overwhelming when life already feels expensive and stressful.

But it is absolutely possible to pay it off with a realistic plan, consistent habits, and patience.

This step-by-step guide on how to pay off 5000 in debt works best when you focus on:

Not perfection.

Because honestly, financial freedom rarely happens through one giant breakthrough moment.

Usually it happens quietly through ordinary decisions repeated long enough to finally change your life.